Below we address the issue of robo trades in the backdrop of crazy markets.

Staying Smart While Partying

Back in April of the last year, we forcasted the tailwinds for the melt-up we are currently enjoying and which hit our “official” radar once the Fed broke out the money printer again in October, at which point we basically screamed “party on!”

But every party animal needs a designated driver—and it’s our role to keep psychologies and portfolios carefully risk-managed, even in a melt-up.

By now, all our subscribers know that when the Fed is “supportive,” markets rise.

No mystery there.

That said, we also warned just two days after our melt-up report that eventually a melt-down follows.

We are not there yet, and are not here to make predictions, as one can neither “fight the Fed” nor predict its unprecedented stimulus’ life-span.

For now, the Fed is in full-on steroid mode.

Nevertheless, we are now in uncharted waters when it comes to predicting the staying power of the Fed’s perpetual money creation and rate suppression.

Rather than tarot cards, we simply watch the market signals, in particular Treasury yields, to warn us of the inevitable “Uh-oh” moment, be it tomorrow or years from tomorrow.

The Terminators Are Back–Robo Trades

Additionally, and as highlighted in our melt-down report, we look carefully at the robots and robo trades to track market risk—i.e. algorithm-based trading (aka “quant strategies” or “robo trades”) which uses computers rather than humans to execute trades.

I called this the “terminator market,” for just like the terminator which Arnold Schwarzenegger made famous, these robo trades and inhuman traders have no emotions, just signals to follow.

This makes robo trades both powerful and dangerous.

So, let’s look at both the power and the dangers of the quant strategies and robo trades looming over our current market party and plan accordingly.

As in 2000, the decade of 2020 has opened with great optimism and market tailwinds. This optimism applies to tech stocks in particular, though not quite as “exuberantly” as the last year of the tech bubble in 2000.

Nevertheless, since 2016, tech has been enjoying its longest run of out-performance and has made up the losses it suffered when the sector tanked in April of 2000, almost 20 years ago.

Are Investors Crazy or Are Robots Just Robots in a World of Robo Trades?

As tech makes a familiar rise with undeniable overvaluations, some are wondering if we are in for another tech crash akin to 2000, or at least a painful sell-off as seen in February of 2018.

For us, over-priced stocks, tech or not tech, are simply the new “abnormal” of the post-08 Fed-rigged markets, and thus over-valuation on its own is not grounds for immediate panic.

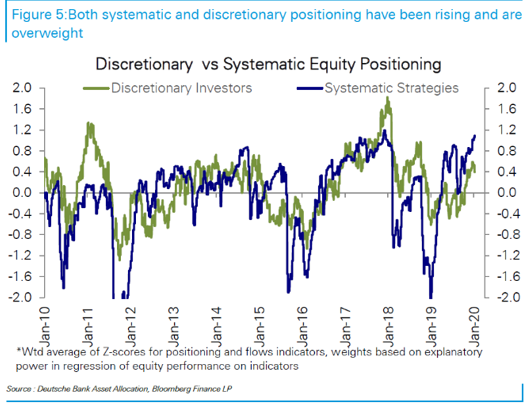

What has us more concerned is the over-complacency we are seeing in the markets and the fact that stocks are now at their highest weightings among the vast majority of investor portfolios as measured by Deutsche Bank’s preferred measuring data.

In fact, the last time investors were this much “all-in” in stocks was on the eve of the great market sell off in February of 2018.

We have learned over the years that the majority of investors tend to act similarly, and by that we mean similarly “badly”—piling in at the tops (like now) rather than patiently waiting to purchase stocks at bottoms, where the real wealth is made.

But can we really blame all these top heavy stock allocations on investor psychology, or is there something more “robotic” at play–i.e. robo trades?

In fact, the flow trackers at both Deutsche Bank and Bloomberg are now reporting that the real reason for all this stock buying is less about retail/discretionary investors (i.e. you and me) and more about the “robots,” namely the systematic quant strategies and robo trades.

Today, the numbers confirm that robo trades account more for the stock enthusiasm than do homo sapiens (i.e. humans)…

Beware of the Terminators and Robo Trades: What We Recommend

This could be dangerous, for as I warned in April of 2019, when “terminators” (i.e. robo trades) take over market buying, they can be a tailwind in the good times but dangerous as hell in a sell-off.

After all, robots don’t think—they just buy or sell based on computerized signals designed by M.I.T grads—and when those robo trades signals say “sell,” the robo sell-offs that follow are brutal, fast and deep.

We saw this not only in February of 2018, but even more so (and more painfully) at the end of that year.

This means informed investors like YOU need to be concerned about another such “mechanized” sell-off in stocks led by robo trades, even in the backdrop of the current melt-up.

In other words stocks in general, and tech socks in particular, are objectively overbought and overweight today. Odds favor a correction at the very least, and very soon.

Or stated even more simply, the “Terminators” and robo trades are back and poised to take a lot of human investors down when their “sell” signals are mathematically triggered. But for such a trigger to happen, we’ll need a big macro even to scare the robots. That can be a long time from now…

In fact, human investor sentiment (i.e. bearishness or bullishness) is currently on the fence, with bulls just barely outnumbering the bears—the real wind behind these stock purchases are coming from robots and robo trades not Jane or John Doe.

Triggers to Watch

So, what might trigger all these terminators and robo trades to sell (rather than buy) at the same time and send your portfolios into a fall?

As always, any sudden change in bond yields will send the robots into a sell-off.

We have said countless times to always keep your eyes on bond yields if you want to measure and track stock direction.

If yields rise for any reason—and there are many reasons they could–markets hate it, not necessarily by the size of the yield spike (at least 2 standard deviations), but by its speed or unexpectedness.

We saw a classic example of this in one trading day last September in the repo markets, prompting a panicked Fed to print at full speed to buy bonds and return yields to their already Fed-suppressed “normal.”

Any spike by 2 standard deviations (i.e. 3-4 basis points) in the span of a month or less could thus be a dangerous trigger, as we saw twice in 2018 and once in 2019. Even David Kostin of Goldman Sachs, paid to be a calming voice, agrees. In fact, we expect the repo markets to get thirsty again in 2020 (i.e. require another Fed bailout of lots and lots of printed dollars).

So, and Again, Should You be Worried?

Great question. For now, and unlike February or October of 2018, the Fed is in full-on “easing mode,” so most would agree that a sudden spike in bond yields is less likely now than it was then.

In short, the Fed is buying every otherwise unwanted bond the Treasury Dept spits out to continue our national debt party.

Such bond support keeps yields in check and thus markets on auto-pilot up and to the right.

The irony, however, is that as bond yields fall due to Fed “accommodation” and optimism for stocks rises, investors tend to sell bonds to buy more stocks. But when they sell bonds, the prices fall and hence the yields (rates) rise, a rise that ultimately circles back to bite stock pricing.

See how weird our Fed-made Twilight Zone is?

In normal markets, you know, the kind where actual supply and demand forces determine bond pricing rather than central bank intervention and robo trades gone rougue, bond yields are usually higher (and prices lower) because investors are happily preferring stocks over bonds.

In Twilight Zone Markets, however, bonds rise on Fed support as stocks rise at the same time.

This correlation can be dangerous, as no one is trading on genuine optimism for the economy, but rather on blind faith in Fed support.

After all, if our economy was really so strong, wouldn’t bond yields normally be a bit higher, as investors comfortably allocate to more stocks?

In the new “abnormal,” however, those days are long gone. And the reason is as simple as it is disturbing: Our markets can’t stomach even a “bit” of a yield (i.e. rate) hike.

Why?

Because we are in debt up to our ears—at record breaking levels of $74 trillion and counting (combined consumer, corporate and government debt).

If the cost of that debt rises (i.e. if yields rise) it’s game over. Full stop.

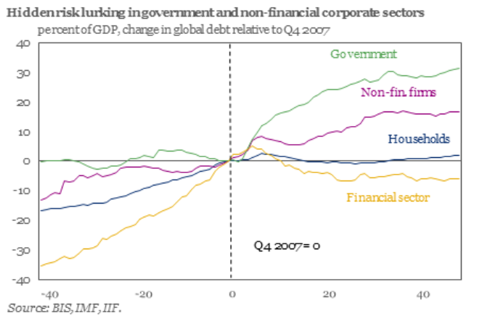

Global Debt Still Hiding Beneath the Waves

Global debt to GDP is now at a staggering 322%, and China, all by itself, has a national debt to GDP level of 310% (according to the Institute of International Finance), with the greatest debt levels stemming from the government sector.

Uh-oh.

In the great crisis of 2008, it was the banks that were over their skis in debt. Since then, the Governments of the world bailed them out, so today, the next crisis lies with the politico’s not the bankers.

But debt is still debt, and cancer is still cancer, and debt is an economic cancer.

Note as well that in the graph above, household debt has not been the great mover, which means that whenever and however the next debt-driven recession comes to fruition, Main Street will once again take a hit for the financial sins of others…

This passing of the debt baton from the banks to the government may explain why so many feel they have nothing to fear—after all, governments, unlike banks or households, can just print money or raise their debt ceilings whenever their debt gets too high.

But we think such optimism is misguided, if for no other reason than common sense and basic ethics suggest otherwise.

And just in case you need a reminder from history, ask the French. And if you like the fantasy of believing we can print for ever, just re-read our report on Modern Monetary Theory, it explains that fantasy away.

As for now, let the melt-up party continue, but for all the reasons (and risks) mathematically proven above, we hope you’re sticking as much to risk management (and Storm Tracker cash allocations) as you are to riding this market wave.

There are lots of rocks beneath those waves…